Income Tax Related Services

Below is a comprehensive list of the income tax services we provide.

We specialize in tax filings, advisory, and compliance solutions tailored to your needs.

Our goal is to ensure seamless and efficient tax management for your business.

ITR-1 is a simplified income tax return form for individuals meeting specific criteria. Here is a brief overview:

Eligibility to File ITR-1

Resident Individuals: This form is only for residents (not ordinarily resident or non-resident).

Income Sources Covered:

Income from salary or pension.

Income from one house property (excluding losses brought forward from previous years).

Income from other sources like interest, dividends, etc. (excluding winnings from lottery and income from horse races).

Exclusions: Individuals with:

Total income exceeding ₹50 lakh.

Agricultural income exceeding ₹5,000.

Income from more than one house property.

Income from business or profession.

Ownership of foreign assets or foreign income.

Tax deduction under section 194N (cash withdrawals).

Key Features of ITR-1

Simple Format: Designed for taxpayers with straightforward income sources.

Pre-filled Data: Information like salary, TDS, and bank details are pre-filled.

E-Filing: ITR-1 can be filed online through the e-filing portal or via assisted filing.

Information Required

Personal Details: PAN, Aadhaar, contact information.

Income Details: Salary slips, bank statements, interest certificates.

TDS Details: Form 16 from employers and Form 26AS for TDS by banks or others.

Tax-Saving Investments: Proofs for deductions under Chapter VI-A (e.g., Section 80C, 80D).

Due Date

For most salaried taxpayers, the due date is 31st July of the assessment year. Delayed filing may attract penalties under Section 234F.

ITR-1 Filing (Sahaj)

The ITR-2 form is designed for individuals and Hindu Undivided Families (HUFs) with income from sources that are more diverse and complex than those allowed under ITR-1. Below is a concise summary:

Applicability of ITR-2

Eligible Individuals and HUFs:

Residents, Non-Residents, and Not Ordinarily Residents can use this form.

Income Sources:

Salary or Pension: Income from employment or pension benefits.

Income from House Property: For multiple house properties.

Capital Gains: Short-term or long-term capital gains from the sale of property, shares, mutual funds, etc.

Income from Other Sources: Interest income, dividends, family pension, lottery winnings, etc.

Agricultural Income: If exceeding ₹5,000.

Other Criteria:

Individuals with foreign income, ownership of foreign assets, or signing authority in foreign accounts.

Taxpayers with income above ₹50 lakh or with assets and liabilities details in India.

Those with income as a partner in a firm (but not business income from proprietary business).

Exclusions: When ITR-2 Cannot Be Filed

Individuals or HUFs with income from business or profession.

Such taxpayers must use ITR-3 or ITR-4.

Taxpayers eligible for presumptive taxation schemes.

Key Features of ITR-2

Detailed Reporting: Requires information on assets, liabilities, and specific financial transactions.

Foreign Income/Assets: Special sections for taxpayers with international income or investments.

Capital Gains Section: Comprehensive schedules for reporting gains from different asset classes.

Information Required for Filing

Personal Details: PAN, Aadhaar, and basic contact details.

Income Details: Salary slips, interest certificates, property details, and capital gains computations.

TDS and Advance Tax: Form 16, Form 26AS, and proof of tax payments.

Investments: Proofs for deductions under Chapter VI-A (e.g., Section 80C, 80D).

Due Date for Filing

The deadline for filing ITR-2 is 31st July of the assessment year unless extended by the government.

ITR-2 is suitable for individuals and HUFs with complex income sources but without business or professional income.

ITR-2 Filing

The ITR-3 form is intended for individuals and Hindu Undivided Families (HUFs) who earn income from business or profession along with other income sources. It is suitable for taxpayers with more diverse and complex financial activities.

Applicability of ITR-3

Eligible Individuals and HUFs:

Business or Professional Income:

Income from proprietary businesses.

Income from professions such as legal, medical, engineering, architecture, etc.

Other Income Sources:

Salary or Pension: Applicable if the taxpayer also has employment income.

House Property: Income from one or multiple house properties.

Capital Gains: Short-term or long-term gains from property, stocks, or other assets.

Income from Other Sources: Interest, dividends, family pension, winnings from lotteries, etc.

Agricultural Income: If exceeding ₹5,000.

Foreign Income and Assets:

Ownership of foreign assets or signing authority in foreign accounts.

Income from foreign sources.

Partners in Firms:

Includes income as a partner from a partnership firm, including salary, bonus, commission, interest, etc.

Exclusions: When ITR-3 Cannot Be Filed

Taxpayers eligible for presumptive taxation schemes under Sections 44AD, 44ADA, or 44AE. Such taxpayers should file ITR-4.

Entities other than individuals or HUFs (e.g., companies, LLPs).

Key Features of ITR-3

Comprehensive Reporting:

Detailed schedules for business and professional income.

Reporting of profit and loss account and balance sheet details.

Income from capital gains and foreign assets.

Deductions and Exemptions:

Claim deductions under Chapter VI-A (e.g., Section 80C, 80D, etc.).

Report exempt income like agricultural income.

Audit Requirements:

Mandatory if turnover exceeds ₹1 crore (₹10 crore if 95% of transactions are digital).

Professionals must get audited if gross receipts exceed ₹50 lakh.

Information Required for Filing

Personal and Business Details: PAN, Aadhaar, and business/profession details.

Income Details: Salary slips, interest certificates, property income, and business income computations.

Financial Statements: Profit and loss account, balance sheet, and turnover details.

Tax Payments: TDS details from Form 26AS, Form 16, and advance tax payments.

Due Date for Filing

For non-audit cases: 31st July of the assessment year.

For audit cases: 31st October of the assessment year.

ITR-3 is suitable for individuals or HUFs with income from business/profession and other diverse sources.

ITR-3 Filing

ITR-4 is a simplified form for individuals, Hindu Undivided Families (HUFs), and firms (excluding LLPs) who opt for presumptive taxation schemes under Sections 44AD, 44ADA, or 44AE of the Income Tax Act. Here's an overview:

Applicability of ITR-4

Eligible Persons:

Individuals, HUFs, and Firms (except LLPs):

Must be residents of India.

Can have income from business or profession under the presumptive taxation scheme.

Income Sources Covered:

Presumptive Income:

Business income under Section 44AD or 44AE.

Professional income under Section 44ADA.

Other Income:

Salary or pension income.

Income from one house property (excluding losses carried forward).

Income from other sources like interest and dividends (excluding winnings from lotteries or horse races).

Turnover/Gross Receipts:

Business turnover should not exceed ₹2 crore.

Professional gross receipts should not exceed ₹50 lakh.

Exclusions: When ITR-4 Cannot Be Filed

Non-residents and non-ordinarily residents.

Individuals or HUFs with income:

Exceeding ₹50 lakh in total.

From more than one house property.

From capital gains.

From speculative businesses (e.g., trading in shares) or winnings from lotteries.

Owning foreign assets or earning foreign income.

Companies, LLPs, and other entities.

Key Features of ITR-4

Presumptive Taxation Scheme:

Under Section 44AD: 8% (or 6% for digital receipts) of gross turnover is considered as income.

Under Section 44ADA: 50% of gross receipts for professionals.

Under Section 44AE: Deemed income from plying, hiring, or leasing goods carriages.

Simplified Reporting:

No need to maintain detailed books of accounts.

No detailed profit and loss account or balance sheet is required.

Deductions:

Deductions under Chapter VI-A (e.g., Section 80C, 80D, etc.).

No additional expenses can be claimed for presumptive schemes.

Information Required for Filing

Basic Details: PAN, Aadhaar, and contact information.

Income Details:

Gross receipts/turnover from business or profession.

Income from salary, house property, and other sources.

Tax Payments:

TDS details from Form 26AS and proof of advance/self-assessment tax paid.

Bank Details: Including all savings and current accounts.

Due Date for Filing

For non-audit cases: 31st July of the assessment year.

For audit cases (if opted out of presumptive scheme): 31st October of the assessment year.

ITR-4 is ideal for small taxpayers using presumptive taxation for businesses or professions, ensuring minimal compliance burdens.

ITR-4 Filing (Sugam)

ITR-5 is a comprehensive income tax return form designed for entities other than individuals who are not required to file ITR-7. It caters to a wide range of taxpayers with business and professional income.

Applicability of ITR-5

Eligible Taxpayers:

Firms: Partnership firms, Limited Liability Partnerships (LLPs).

Associations of Persons (AOPs) and Bodies of Individuals (BOIs).

Artificial Juridical Persons (AJPs).

Co-operative Societies and Local Authorities.

Business Trusts and Investment Funds.

Other Entities not required to file ITR-6 or ITR-7.

Income Sources Covered:

Business or Profession: Includes income from operations and professional services.

Capital Gains: Short-term or long-term gains.

House Property: Income from one or more properties.

Other Sources: Interest, dividends, etc.

Exclusions: When ITR-5 Cannot Be Filed

Individuals and HUFs: These taxpayers file ITR-1 to ITR-4.

Companies: Must file ITR-6.

Charitable or Religious Trusts and Institutions: Required to file ITR-7.

Key Features of ITR-5

Detailed Reporting:

Profit and loss account, balance sheet, and details of business activities.

Schedule for capital gains, foreign income, and tax-saving investments.

Deductions and Exemptions:

Deductions under Chapter VI-A (e.g., Section 80C, 80D).

Exemptions under various provisions of the Income Tax Act.

Tax Audit Compliance:

Audit report submission under Section 44AB, if applicable.

Partner/Member Details:

Information about partners (for firms) or members (for AOPs/BOIs).

Information Required for Filing

Entity Details: PAN, name, address, and registration details.

Income Details: Business income, house property income, capital gains, and other sources.

Tax Payment Details:

TDS and TCS details from Form 26AS.

Self-assessment and advance tax payments.

Financial Statements: Profit and loss account, balance sheet, and details of assets and liabilities.

Details of Partners or Members: Share in profits, remuneration, and interest paid.

Due Date for Filing

Non-Audit Cases: 31st July of the assessment year.

Audit Cases: 31st October of the assessment year.

ITR-5 is suitable for firms, LLPs, and other entities with business income or professional income who are not individuals or companies.

ITR-5 Filing

ITR-6 is the income tax return form designed specifically for companies (excluding those claiming exemption under Section 11) to report their income, deductions, and taxes.

Applicability of ITR-6

Eligible Taxpayers:

Companies:

Indian companies.

Foreign companies operating in India.

Income Sources Covered:

Income from business or profession.

Income from house property.

Capital gains (short-term and long-term).

Income from other sources, such as interest and dividends.

Foreign income and foreign assets.

Exclusions: When ITR-6 Cannot Be Filed

Companies Claiming Exemption under Section 11:

This section applies to charitable or religious trusts.

Such companies should file ITR-7.

Other Entities:

Firms, LLPs, individuals, and HUFs must file ITR-1 to ITR-5.

Key Features of ITR-6

Electronic Filing:

ITR-6 must be filed electronically and verified using digital signatures.

Detailed Schedules:

Includes detailed reporting of income, deductions, exemptions, and taxes paid.

Separate schedules for MAT (Minimum Alternate Tax) and AMT (Alternate Minimum Tax).

Foreign Reporting:

Details of foreign income and assets.

Transactions with foreign entities.

Tax Computation:

Comprehensive schedules for claiming tax deductions, exemptions, and MAT credits.

Information Required for Filing

Basic Company Details:

PAN, incorporation details, CIN (Corporate Identification Number), and type of company.

Income and Financial Data:

Details of income from business, capital gains, house property, and other sources.

Profit and loss account and balance sheet details.

Tax Payment Details:

TDS (Form 26AS), advance tax, and self-assessment tax payments.

Exemptions and Deductions:

Section 10 exemptions and Chapter VI-A deductions (e.g., 80G, 80JJAA).

MAT/AMT Computation:

Calculation of Minimum Alternate Tax under Section 115JB.

Due Date for Filing

Non-Audit Cases: 31st July of the assessment year.

Audit Cases: 31st October of the assessment year.

ITR-6 is mandatory for companies except those claiming tax exemption as charitable or religious entities.

ITR-6 Filing

ITR-7 is the income tax return form designed for specific entities, including trusts and institutions, that claim exemptions under the Income Tax Act or are subject to specific tax reporting requirements.

Applicability of ITR-7

Eligible Taxpayers: Entities required to file ITR-7 include those filing returns under the following sections:

Section 139(4A): Income from property held under trust for charitable or religious purposes.

Section 139(4B): Income from a political party.

Section 139(4C): Entities such as:

Research associations.

News agencies.

Associations or institutions for controlling or improving specific professions.

Universities, colleges, or other institutions whose income is exempt under specific provisions.

Section 139(4D): Universities, colleges, or other institutions not required to furnish returns of income/loss under any other provision.

Section 139(4E): Business trusts.

Section 139(4F): Investment funds under Section 115UB.

Income Sources Covered:

Income from voluntary contributions (e.g., donations).

Income from house property.

Income from capital gains.

Income from other sources like interest and dividends.

Exclusions: When ITR-7 Cannot Be Filed

Individuals, HUFs, and companies not falling under the specified sections.

Entities not claiming tax exemptions or deductions under the applicable sections.

Key Features of ITR-7

Section-Specific Filing:

Separate schedules for reporting based on the applicable section (e.g., 139(4A), 139(4B)).

Charitable/Exempt Entities:

Detailed reporting of activities, funds, and income under trust/institution rules.

Political Parties:

Disclosure of donations and other receipts.

Business Trusts/Investment Funds:

Reporting of income distributed and exempt income.

Information Required for Filing

Basic Details:

PAN, registration details, and type of entity.

Income and Expenditure:

Income from donations, investments, and other sources.

Expenditure incurred for charitable or specified purposes.

Tax Exemptions:

Details of exemptions claimed under relevant sections (e.g., Section 11, Section 13).

Tax Payments:

TDS, advance tax, and self-assessment tax details.

Foreign Contributions (if any):

Disclosure of foreign contributions and compliance under the Foreign Contribution Regulation Act (FCRA).

Due Date for Filing

Entities Requiring Audit: 31st October of the assessment year.

Other Cases: 31st July of the assessment year.

ITR-7 is tailored for entities like trusts, political parties, and institutions claiming tax exemptions or operating under specific regulatory requirements.

ITR-7 Filing

TDS (Tax Deducted at Source) return filing is a mandatory compliance requirement for deductors under the Income Tax Act, 1961. It involves the submission of detailed information regarding tax deducted and deposited to the government within prescribed timelines. The process ensures transparency and accurate credit of TDS to the payee’s account.

The key steps in TDS return filing include:

Collection of Details: Gather details of payments made and TDS deducted during the quarter, including PAN of deductees, amount paid, and tax deducted.

Challan Payment: Ensure timely payment of TDS using the appropriate challan (Challan No. ITNS 281) within due dates.

Preparation of Return: Use the prescribed file formats (Form 24Q for salaries, Form 26Q for non-salaries, Form 27Q for payments to non-residents, etc.) and validated data to prepare the return.

Validation: Validate the TDS return file using the File Validation Utility (FVU) provided by NSDL.

Submission: Upload the validated file through the TIN-FC or the Income Tax e-filing portal.

Correction: Post-submission, corrections (if any) can be made using a revised return to ensure accurate reporting.

Timely filing of TDS returns ensures compliance, prevents penalties, and enables smooth credit of TDS to deductees. Penalties for non-filing or incorrect filing include late filing fees under Section 234E and penalties under Section 271H.

For professional assistance in filing accurate and timely TDS returns, ensuring compliance with all statutory requirements, contact us today!

TDS Returns Filing

A revised return can be filed under Section 139(5) of the Income Tax Act when an assessee discovers an omission or wrong statement in their original return filed under Section 139(1) or in a belated return under Section 139(4).

Key Aspects:

Eligibility:

The original or belated return must have been filed within the due date as prescribed under Section 139.

Errors or omissions that are rectifiable, such as incorrect details or missed disclosures, qualify for revision.

Timeline:

A revised return can be filed up to three months prior to the end of the relevant assessment year or before the completion of assessment, whichever is earlier.

Procedure:

Use the same Income Tax Return (ITR) form as used for the original return.

Select the appropriate option to indicate it is a revised return.

Provide details of the original return, such as acknowledgment number and filing date.

Multiple Revisions:

A return can be revised multiple times within the permissible time frame.

Consequences of Revision:

Replacing the original return: Once revised, the earlier return is treated as withdrawn.

Penalty for Concealment: If false information is discovered later, penalties may apply.

Assessment after Revision:

The revised return is considered by the Assessing Officer (AO) while making assessments.

Special Scenarios:

Returns filed in response to notices under Sections 142(1) or 148 cannot be revised.

This provision ensures that taxpayers have an opportunity to rectify errors in a timely manner to avoid penalties or scrutiny.

Revised Return Filing

TDS corrections refer to the process of rectifying errors or inaccuracies in previously filed TDS returns to ensure compliance and accurate credit of tax to deductees. Corrections are essential when discrepancies like incorrect PANs, challan details, or tax amounts are identified, as they can lead to notices or mismatched credits.

The process involves:

Identification of Errors: Review filed TDS returns to pinpoint errors such as incorrect PAN, challan details, deduction amounts, or section codes.

Accessing the TRACES Portal: Log in to the Tax Deduction and Collection Account Number (TAN) account on the TRACES portal to initiate corrections.

Downloading the Conso File: Retrieve the consolidated file of the relevant TDS return from TRACES. This file contains details of the original return necessary for making corrections.

Making Corrections: Use a utility like RPU (Return Preparation Utility) or any approved software to modify the errors in the return. Ensure all changes are accurate and verified.

Validation: Validate the corrected file using the File Validation Utility (FVU) provided by NSDL.

Submitting the Revised Return: Upload the corrected return through the TRACES portal or submit it at a TIN Facilitation Center.

Acknowledgment and Monitoring: Obtain the acknowledgment for the revised return and monitor its status to ensure acceptance by the department.

TDS correction is a critical aspect of compliance, as unresolved errors can result in penalties or hinder tax credit for deductees.

For expert guidance and seamless TDS correction services, ensuring compliance and accuracy, contact us today!

TDS Corrections

Income Tax Notice Response

Dealing with income tax notices requires a systematic and professional approach to ensure compliance and resolution. When a notice is received, the first step is to verify its authenticity and review its details to understand the reason for issuance, whether it pertains to underreporting of income, mismatches in TDS, or other compliance issues. We promptly inform clients and explain the implications of the notice, collecting all necessary documentation such as tax returns, financial statements, and supporting evidence. This ensures a thorough understanding of the situation.

Next, we prepare a comprehensive and precise response tailored to address the specific queries or discrepancies highlighted in the notice. Our team ensures that all supporting documentation is included and unnecessary details are avoided, maintaining clarity and professionalism in communication. Once the response is finalized, it is submitted within the prescribed timeline through the appropriate mode, such as the Income Tax Portal, to avoid penalties or delays. An acknowledgment is obtained to confirm submission.

We continuously monitor the case status and stay responsive to any additional queries or follow-up requirements from the tax authorities. If representation is necessary, our skilled professionals represent clients effectively in hearings or meetings, ensuring their interests are safeguarded. After the resolution, we provide closure confirmation and maintain detailed records of the process for future reference.

Beyond resolving notices, we also advise clients on preventive measures to minimize the likelihood of future issues. Our services include regular tax health checks and compliance reviews, helping businesses and individuals stay proactive and compliant with tax regulations.

If you have received an income tax notice or need assistance with your tax compliance, we are here to help. Contact us for expert guidance and comprehensive support in managing all aspects of income tax notices and related services.

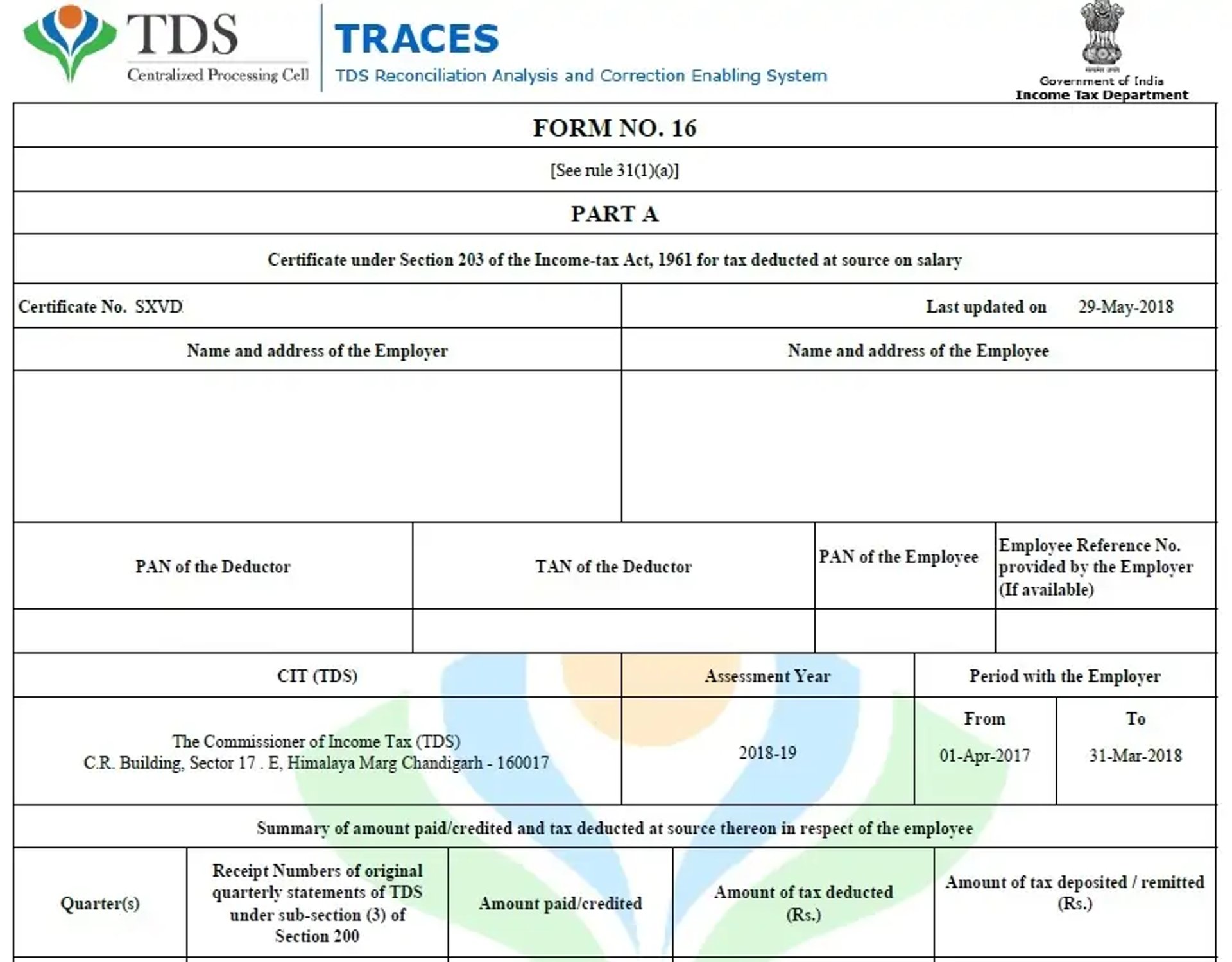

Form 16 Issuance

Form 16 is a crucial document provided by employers to their employees, certifying details of salary paid and TDS deducted during a financial year. It helps employees file their income tax returns and serves as proof of tax compliance. The process for issuing Form 16 involves the following steps:

1. Data Compilation

Gather comprehensive details of each employee's salary, allowances, deductions, and tax calculations for the financial year.

Ensure the accuracy of TDS deducted and deposited to the government.

2. Generation of Form 16

Part A: Download from the TRACES portal after verifying the TDS returns filed (Form 24Q). This section contains details of the TDS deducted, deposited, and PAN/TAN of the employer and employee.

Part B: Prepare internally or using payroll software. It includes a detailed breakup of salary components, exemptions under Section 10, deductions under Chapter VI-A, and taxable income.

3. Verification

Cross-check the information in Form 16 against payroll records and filed TDS returns to ensure consistency and correctness.

Resolve discrepancies, if any, before finalizing the forms.

4. Issuance to Employees

Distribute the signed and validated Form 16 (Part A and Part B) to employees by the due date, generally on or before June 15 of the following financial year.

Provide both digital (PDF) and physical copies, ensuring accessibility for employees.

5. Support and Assistance

Offer guidance to employees on how to interpret Form 16 and use it for filing their income tax returns.

Employers must ensure timely and accurate issuance of Form 16 to avoid penalties and enhance employee satisfaction. For seamless payroll management and Form 16 issuance services, contact us today!

Net Worth Certificate Issuance Facilitation Services

A Net Worth Certificate (NWC) is a document issued by a Chartered Accountant (CA) that certifies an individual's or entity’s financial worth, calculated as the difference between total assets and liabilities. It is often required for loan applications, visa purposes, or financial due diligence. The process of issuance involves the following steps:

1. Collecting Financial Information

Gather details of all assets, including immovable properties (land, buildings), movable assets (vehicles, gold, and other valuables), investments (shares, mutual funds), bank balances, and other personal assets.

Compile details of liabilities, such as loans, credit card dues, and any other outstanding debts.

2. Verification of Documents

The CA verifies ownership and valuation documents for the assets and liabilities provided.

Supporting evidence like property deeds, valuation certificates, investment statements, bank account balances, and loan statements is thoroughly examined to ensure accuracy and authenticity.

3. Valuation of Assets and Liabilities

Assess the fair market value of assets, ensuring valuations are recent and compliant with applicable standards.

Deduct liabilities to determine the individual’s or entity's net worth.

4. Drafting the Certificate

Prepare the certificate on the CA’s official letterhead, clearly stating the name, address, and financial details of the individual/entity.

Include the computation of net worth with a detailed breakup of assets and liabilities.

5. Certification and Issuance

The CA signs the certificate and affixes their seal, confirming its authenticity.

Provide the signed certificate to the individual or entity for their intended use.

6. Compliance and Record-Keeping

Maintain a record of the certificate and supporting documentation for future reference and compliance requirements.

For accurate and professionally prepared Net Worth Certificates, contact us for reliable assistance tailored to your needs!

+91 9885904075

Contact Us

Our Services

Quick Links

PAN Related Services

Income Tax Services

GST Related Services

Labour Law Services

International Taxation

Book keeping Services

Payroll Compliance and processing Services

Business Process Transformation Services

Business Process Review and Gap Analysis

Preparation of Financial Statements

Sole Proprietorship registration

Partnership Registration

LLP Incorporation

Company Incorporation

Filing of Annual Returns And financial Statements

Maintenance of Statutory Registers and Records

Compliance with Board and Shareholder Meetings

Assistance with Dematerialization of Securities

Closure of Companies and LLPs

MSME Registration and Compliance

Others

Stock Audit Facilitations

Payroll Audit Facilitations

Tax Audit Facilitations

Mergers and Acquisitions Advisory

Due Diligence Reports

Financial Modelling

Valuations

Corporate Finance Advisory

Legal Drafting and Advisory

Secretarial Compliances

Business Certifications

Liaisoning Services

Copyright © 2025 Advizin private limited